L'optimisation de la gestion des notes de frais et son impact sur la trésorerie

La gestion des notes de frais est une composante essentielle de la comptabilité d'une entreprise. Une mauvaise gestion... En lire plus

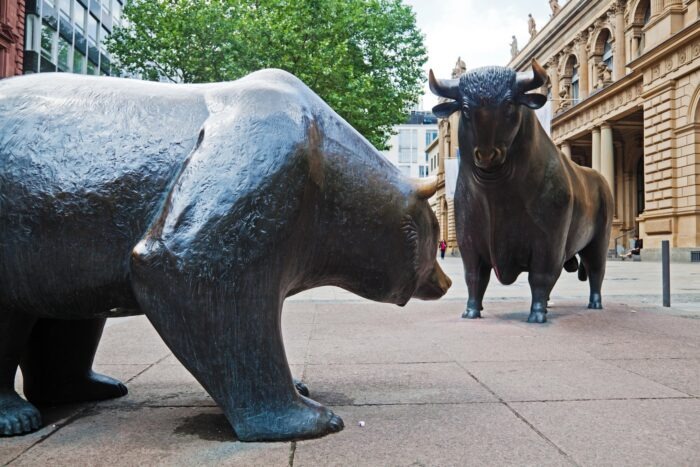

Somewhere between Elon Musk becoming the world's first trillionaire and Sam Altman still figuring out how to turn a profit, 2026 quietly became the year Wall Street ran out of superlatives.

SpaceX, Anthropic, and (maybe, eventually) OpenAI have turned the public markets into a runway for the most consequential IPO season in a generation.

Between rockets, chatbots, and a valuation arms race that would make a dot-com investor blush, one has to ask: are we watching the birth of a new industrial era, or the most expensive game of musical chairs ever played?

Let's start with the one that already landed. On June 12, SpaceX priced its IPO at $135 a share, raising $75 billion in what instantly became the largest public offering in history. Shares popped nearly 20% on debut, pushing the company's market cap above $2 trillion and, in the process, minting Musk as the planet's first trillionaire.

For context, this is a company that lost close to $5 billion in 2025 and whose "AI segment" - the newly absorbed xAI - is burning cash at a pace that would make most CFOs faint. CFRA slapped a "sell" rating on it days after the debut; New Street Research countered with a price target above where it is trading, arguing you simply have to zoom out twenty years to make the maths work. Somewhere in between those two views lies the actual story.

Then there's Anthropic, which confidentially filed its own draft S-1 on June 1 - deliberately getting ahead of OpenAI - just days after closing a $65 billion round at a $965 billion valuation, comfortably surpassing its main rival. The company behind Claude says its revenue run-rate has rocketed to roughly $47 billion, up from $10 billion a year earlier, driven largely by Claude Code and enterprise adoption. Bankers have reportedly told both labs that whoever lists first gets to set the template the market will use to judge the entire AI sector.

And then there is OpenAI, the company that arguably started this whole circus with ChatGPT, which filed its own confidential paperwork on May 22. Except OpenAI's story reads differently: still unprofitable, reportedly burning through cash at a pace unprecedented for a company its size, and - according to recent reporting - now possibly pushing its listing into 2027 rather than racing to market this year. Its CFO has said the company would rather stay private a little longer if it means getting the reporting infrastructure right. Translation: even Sam Altman knows Wall Street doesn't forgive sloppy homework.

If this feels like déjà vu, it is because we have been here before - just replace Oracle-Nvidia-CoreWeave circularity with Musk-Anthropic-SpaceX circularity. Anthropic, for instance, has agreed to pay SpaceX $1.25 billion a month through 2029 for compute at its Colossus data centre in Memphis. Tesla owns a chunk of SpaceX shares. SpaceX owns xAI. Everyone seems to be everyone else's customer, landlord, and shareholder simultaneously. It's not fraud, it is just an ecosystem so tightly wound that a wobble in one corner could ripple through all three.

For index investors, this is genuinely new territory. A $2 trillion SpaceX joining the Nasdaq, alongside a potential trillion-dollar Anthropic and OpenAI, means passive funds - the ones sitting quietly in most people's pension pots - suddenly carry enormous, concentrated bets on companies that, by traditional metrics, would never qualify for blue-chip status. None of the three is reliably profitable. Anthropic just posted its first profitable quarter, reportedly around $559 million in Q2 operating income against nearly $11 billion in revenue - genuinely impressive growth, but still a rounding error next to the capital these companies are committing to data centres, chips, and compute.

For AI companies broadly, the message is louder still: public markets are now open as a financing tool for the arms race, not just private mega-rounds. That's a double-edged sword. It unlocks retail capital - SpaceX controversially allocated roughly 30% of its offering to individual investors rather than the usual single digits - but it also exposes ordinary shareholders to volatility that used to be the exclusive privilege of venture capitalists with padded balance sheets.

For consumers, the effects will likely be indirect but real: pressure to monetise faster (subscription price hikes, tighter free tiers, more aggressive enterprise upselling) as public markets demand quarterly accountability that private board meetings never did.

The bullish case: all three IPOs perform reasonably well, capital markets absorb the costs of the AI buildout, and public ownership actually disciplines these companies into achieving better unit economics than their private, cash-flush years allowed.

The bearish case: one IPO stumbles badly — most likely OpenAI, given its cash burn — dragging sentiment down across the sector and triggering a broader repricing of “AI premium” valuations, not unlike what followed the dot-com peak.

The messy middle: all three list successfully, trade with wild volatility for 12–18 months, and the real verdict does not arrive until 2028 or so, when lock-ups expire, infrastructure bills come due, and we finally see whether the revenue curves catch up with the spending curves.

Whichever way it goes, one thing already seems clear: 2026 did not just give us new stocks to buy. It gave the entire AI industry a permanent quarterly report card — and not everyone is going to like their grades.

By the same author:

🧾 Les chroniques des horlogers de Genève : François Czapek

🧾 The Hitchhiker's Guide to the AI Galaxy

🧾 Rolex Sea-Dweller: The Toolest Watch Rolex Has Ever Made

🧾 Resetting Omega: Charting a New Course with Old Compass

🧾 A Pole in Space: Sławosz’s Odyssey

Images:

Le siège social de SpaceX à Hawthorne, Californie — Image de wirestock_creators

A writer and analyst with a keen interest in the intersection of science, philosophy, and culture.